The lowest value in the history of the Czech market

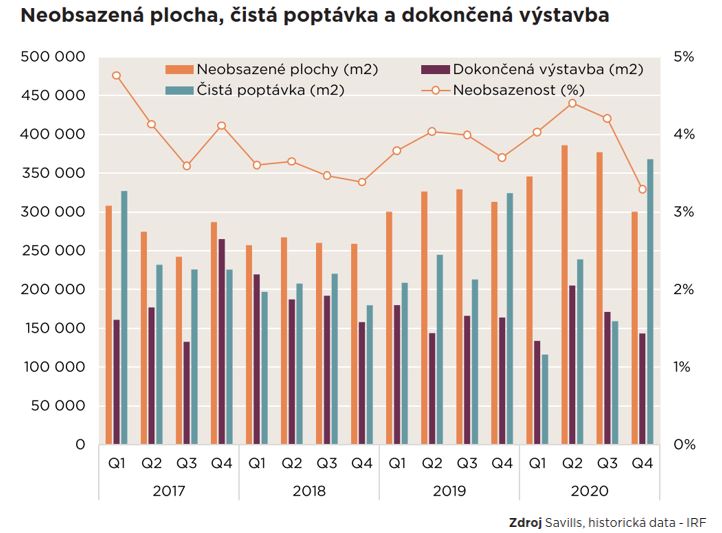

The vacancy rate in the Czech Republic fell to 3.3%, which is the lowest value in the history of the Czech market. It has fallen by 111 basis points (bps) since the middle of the year and has fallen by 41 bps since the beginning of the year. In Prague, the share of unleased space decreased from 2.7% in mid-2020 to 1.5% at the end of the year. This corresponded to 49,300 square meters.

At the end of 2020, a total of 692,500 square meters of industrial space was under construction in the Czech Republic. Slightly less (by 1%) than 12 months ago. 26% of these spaces were buildings already built in the rough construction phase.

In the last quarter of 2020, construction began on several completely new sites

Lenka Pechová, senior research analyst Savills CR and SR, says: “Despite the persistently high level of economic uncertainty, new construction of industrial real estate across the country was driven by rising occupancy rates and demand for non-existent larger warehouse units. In the last quarter of 2020, construction began on several completely new sites. Especially near Prague and in the Moravian-Silesian region."

Rental activity in the industrial real estate market showed strong results. This proves the resilience of this real estate segment even during a pandemic. Total demand reached 829,000 square meters in the second half of the year. Thus, 14% more than in the second half of 2019. Total rental activity in 2020 reached 1,544,600 square meters, 5% more than in 2019. Net rental activity for the last six months of 2020 was at 527,400 square meters, almost the same as in the second half of 2019. The total net rental activity in 2020 reached 882,600 m2 and was only 11% below the activity recorded in 2019.

Chris LaRue, Head of Industrial Real Estate Leasing, Savills CR and SR, adds: “Net leasing activity was significantly boosted in 2020 by demand from the e-commerce sector and, to some extent, the retail sector. The growth of e-commerce will continue in 2021, although there will probably be a slight slowdown compared to 2020. Demand will continue to be significantly supported by the activity of logistics companies and there may also be requirements for leasing space from companies operating in the automotive sector. "

Source:// Systémy logistiky